The UEMOA’s January 2026 economic outlook report delivers a stark verdict: while the West African Monetary Union’s banking sector reaches symbolic milestones, it is increasingly undermined by surging risks. At the heart of this turmoil, Niger stands out with an unprecedented non-performing loan rate, epitomizing a widening regional divide.

The Niger Paradox: A Warning Signal for Regional Stability

Despite UEMOA’s efforts to stabilize its financial system, Niger remains the most fragile link in the regional banking chain. Even marginal improvements fail to mask the country’s precarious position, where credit defaults continue to escalate.

A Record-Breaking Default Rate

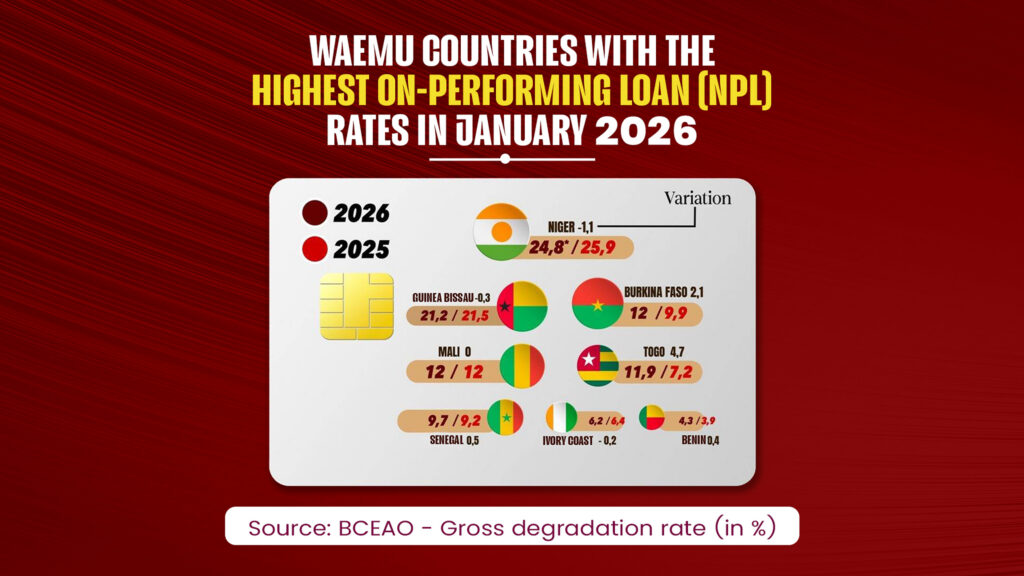

In January 2026, Niger’s non-performing loan rate soared to 24.8%, the highest in the Union. This means nearly one in four loans granted in Niger is now in default—a figure that, while slightly down from 25.9% in 2025, still dwarfs regional averages. The structural vulnerability driving this crisis stems from persistent security threats and political instability, creating an environment where financial risks are amplified.

A Divided Union: Coastal Stability vs. Sahelian Instability

The January 2026 data underscores a widening economic chasm between coastal nations and the Sahelian bloc, where Niger serves as the epicenter of the crisis.

The Sahel Under Strain

- Mali and Burkina Faso: Both countries report a 12% default rate, with Burkina Faso experiencing a sharp annual increase of +2.1 percentage points—a trend that raises red flags.

- Guinea-Bissau: Remains in critical territory with a 21.2% non-performing loan rate.

The Coastal Bloc’s Relative Resilience

In contrast, coastal economies demonstrate greater financial stability, though not without concerns:

- Benin: Leads the Union with the lowest default rate at 4.3%.

- Ivory Coast & Senegal: Maintain stability with rates of 6.2% and 9.7%, respectively.

- Togo’s Outlier: Defies regional trends with a sudden spike, jumping from 7.2% to 11.9% (+4.7 points).

Systemic Pressures: Credit Growth Stalls Amid Rising Defaults

While total credit to the regional economy surpassed 40.031 trillion FCFA—a historic milestone representing a 4.7% annual increase—the momentum appears faltering. Non-performing loans have ballooned to 3.631 trillion FCFA, pushing the coverage ratio down to 59%. This means banks are struggling to keep pace with losses as defaults surge.

Banks Tighten the Reins

Faced with escalating risks in countries like Niger, financial institutions are adopting defensive strategies:

- Stricter lending conditions: Higher personal contributions and tighter collateral requirements.

- Selective lending: Banks prioritize balance sheet safety over credit expansion, risking a slowdown in funding for local SMEs and SMEs.

As the UEMOA banking system navigates this pivotal moment in early 2026, the Niger crisis and the spread of risk across the Sahel demand heightened vigilance to avert a potential liquidity crunch.